One of the most common questions I get from investors is:

“Should I invest my entire $100,000 at once or break it up into smaller amounts over time?”

This decision—between lump sum investing (LSI) and dollar-cost averaging (DCA)—is particularly relevant during periods of market volatility, geopolitical uncertainty, or economic shifts. But here’s the truth:

- There is a statistically correct answer based on historical data

- There is also a psychological answer—the best strategy is the one you can stick with

This guide will break down both perspectives so you can make an informed decision.

Understanding dollar-cost average versus lump sum

| Strategy | How it works | Key benefit | Main risk |

|---|---|---|---|

| Lump sum investing (LSI) | Invest the entire amount at once | Historically, markets rise over time, so money works longer | Short-term market drops could reduce portfolio value |

| Dollar-cost averaging (DCA) | Invest in smaller amounts over time (e.g., $10,000 per month for 10 months) | Reduces short-term risk, smooths out volatility | If markets rise, delayed investing may lead to missed returns |

Both strategies get you into the market, but they work differently based on market conditions and investor psychology.

DCA or lump sum – math example

A Vanguard study found:

- 68% of the time, lump sum investing (LSI) outperformed dollar-cost averaging (DCA)

- 69% of the time, DCA outperformed leaving money in cash

- 70% of the time, LSI outperformed leaving money in cash

Why does LSI win most of the time?

- Markets go up more often than they go down → Investing earlier captures more growth

- Dividends start compounding sooner → In Australia, dividends are a significant part of returns

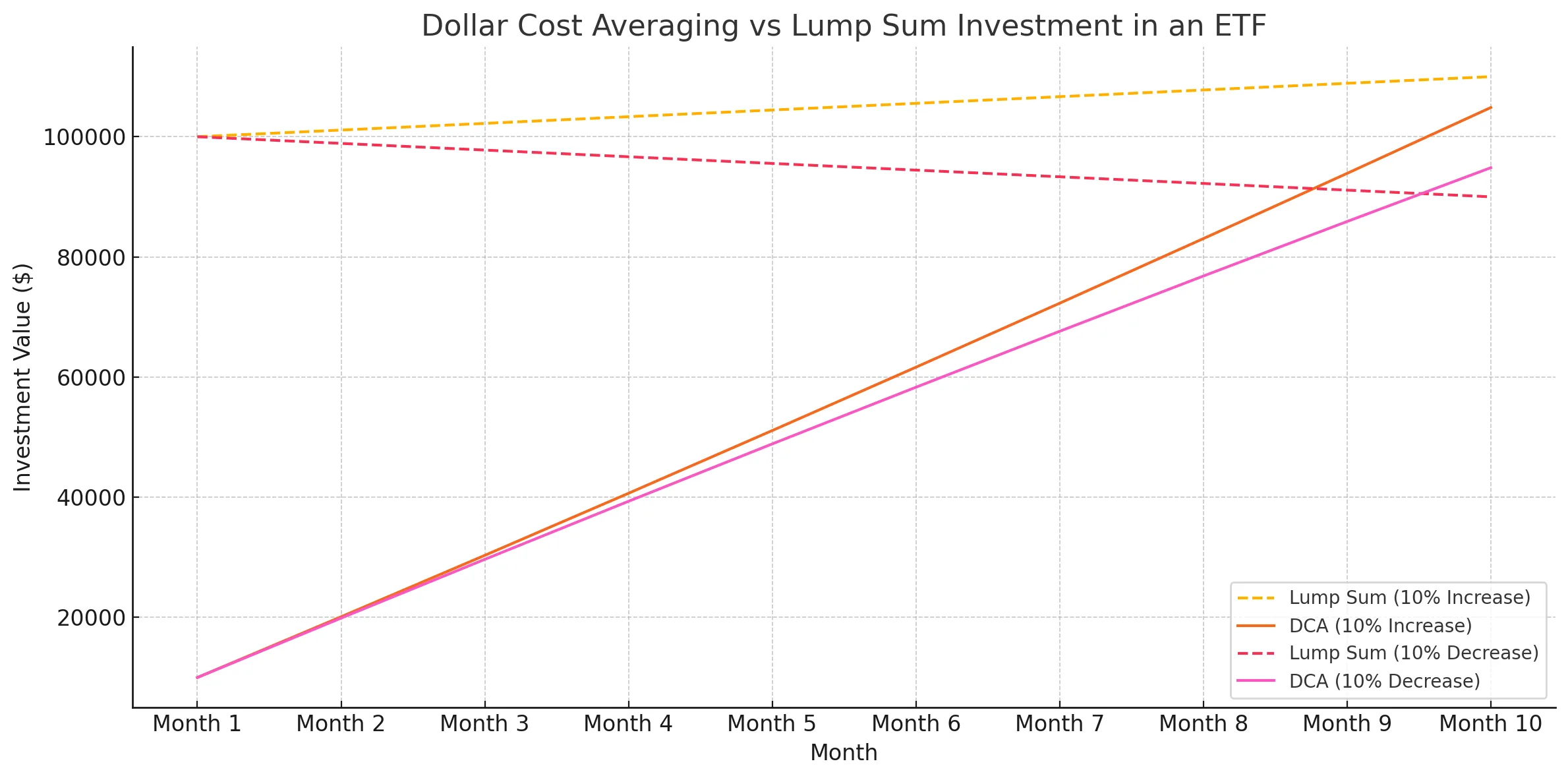

Example: Lump sum vs. dollar-cost averaging returns over ten months

In this scenario we have compared lump sum investing an amount of $100,000 vs dollar cost averaging ten $10,000 parcels. We have shown two scenarios for both, an increase in the market of 10% and a decrease of 10%. As you can see, even in the decrease of 10% the dollar cost averaging approach is only marginally better.

Risk of dollar-cost averaging – what’s better for me?

While lump sum investing (LSI) is statistically better, dollar-cost averaging (DCA) can help reduce anxiety if you’re nervous about market movements.

When to use lump sum investing (LSI):

- You understand that short-term market drops are normal

- You don’t want to delay potential gains

- You want your money working for you immediately

When to use dollar-cost averaging (DCA):

- You’re uncomfortable investing a large sum at once

- You want to spread out your risk in case of a short-term market drop

- You tend to react emotionally to market swings and prefer a gradual approach

Important note: The biggest mistake is stopping DCA because of fear. If you choose DCA, stick to the plan and keep investing regularly.

Should I just wait before investing?

Peter Lynch, one of the most successful fund managers, said:

“More money has been lost waiting for market corrections than in market corrections themselves.”

And, our favourite, Morgan Housel, author of The Psychology of Money, explains:

“Volatility is the price of admission to long-term investing.”

If you sit on the sidelines and wait for the “perfect time” to invest you’ll never end up investing. As my good friend, John Addis says, there’s always something to worry about.

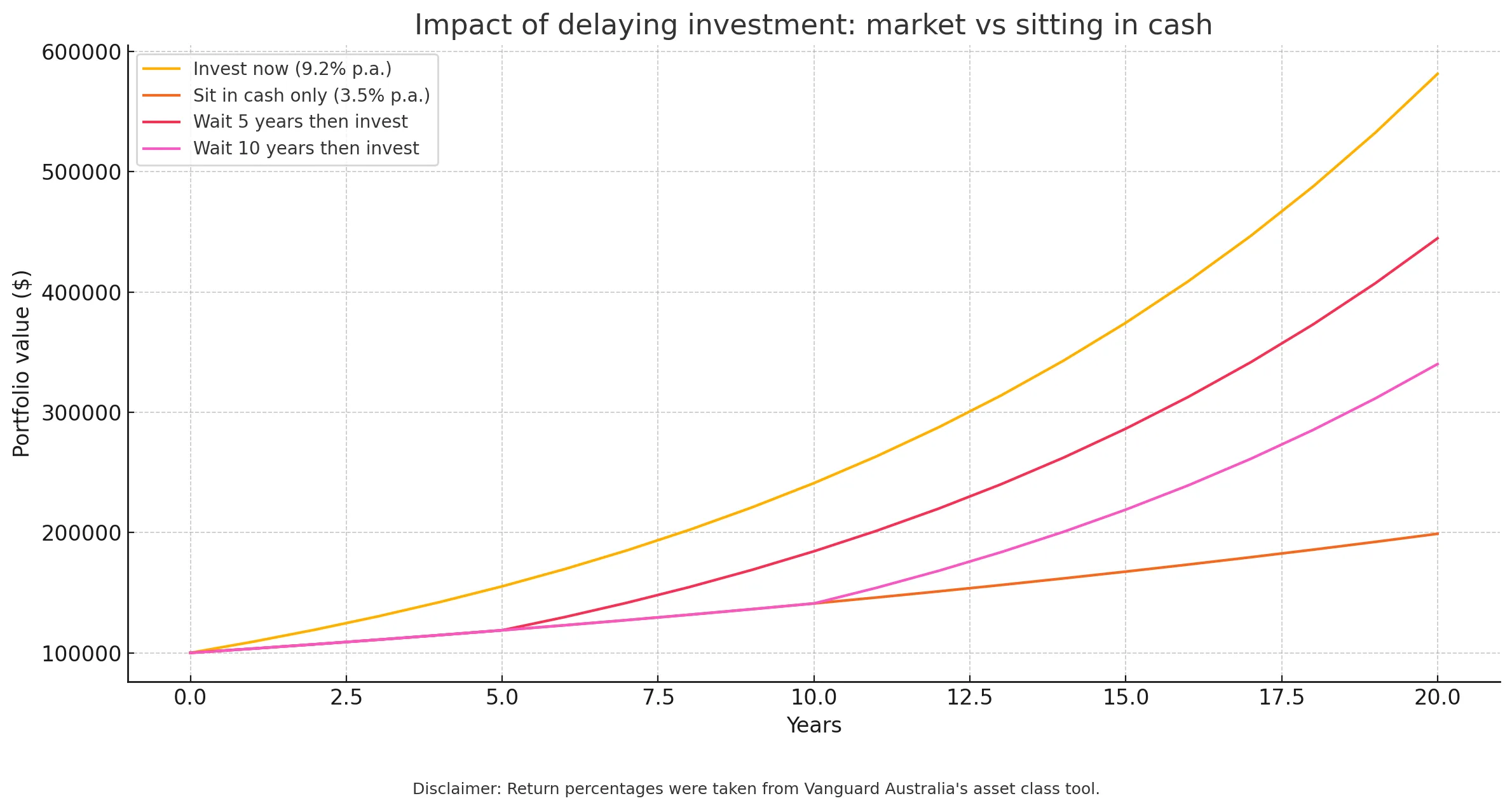

Example: Holding cash vs. investing in the market

Key takeaway: The longer you wait, the greater the opportunity cost.

Best strategy for investing in ETFs

| If you prioritise… | Best strategy |

|---|---|

| Maximising returns | Lump sum investing |

| Reducing short-term risk | Dollar-cost averaging |

| Avoiding emotional investing | Dollar-cost averaging |

| Minimising opportunity cost | Lump sum investing |

Ultimately, the best strategy is the one you can stick with. Whether you choose LSI or DCA, the most important thing is to start investing and stay invested.

DCA or lump sum: key takeaways

- 68% of the time, lump sum investing outperforms dollar-cost averaging

- Dollar-cost averaging is better than waiting in cash—just stay committed

- Markets go up more often than they go down—investing earlier captures more gains

- Your decision should match your risk tolerance—psychology matters

- The worst decision? Becoming paralysed by the choice and not investing at all

How can you dollar cost average into a Rask Invest account? Check out this guide

How we invest

At Rask Invest, we recommend choosing the strategy that aligns with your risk tolerance and investing style. If you’re comfortable, lump sum investing historically leads to better results. If you prefer to ease into the market, dollar-cost averaging is a great alternative—as long as you stick to the plan.

The key thing for our portfolios is that they are designed to be resilient and diversified, straight out of the gate. Meaning, if you plan to invest the way we do – sensible, long-term, diversified – it doesn’t matter much which option you follow. What matters is you invest and stay invested.

If you’re worried about being able to stay invested, please consider getting help from a professional investment firm. Why? Mistakes can be very costly. Our safe technology, handy automation features, professional portfolio management, low fees, full tax reporting and automation make it easy to get started and stay invested. Whether the market rises or falls over the next 12 months, the long-term outlook is bright.

Need help deciding which strategy to follow?

If you need a hand thinking about how to invest for the long term, you can view our portfolios, read our investment manual, or book a call with me to discuss your options. Finally, I encourage you to jump into our Community. It’s a great place to chat with like-minded investors. You’ll find Owen and me there too.