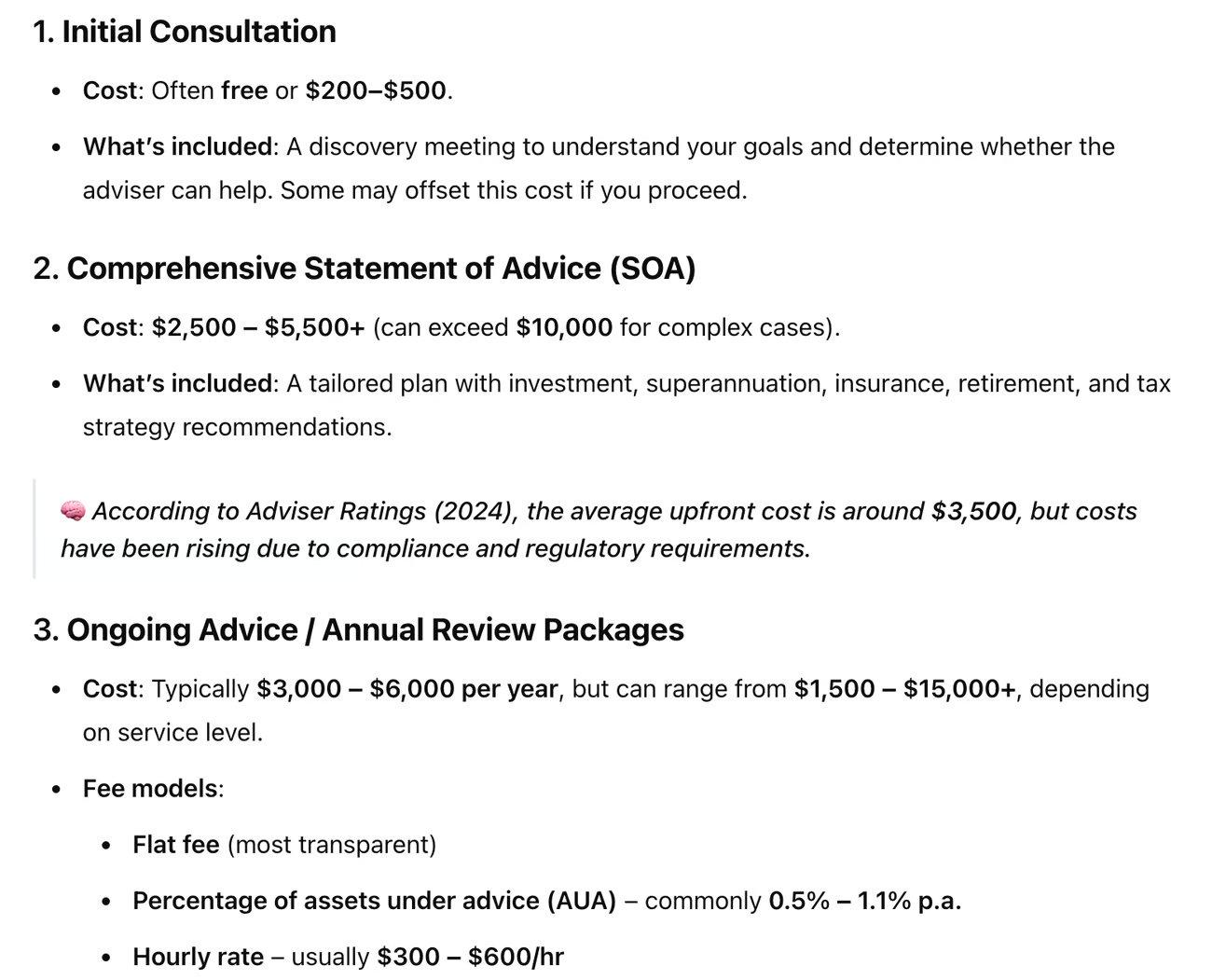

If you ask “Chad” (ChatGPT) or Dr Google, “what is the average cost of financial planning in Australia?” it will come back with something like this financial planning table of costs:

This answer reminds me of the story of the 6-foot man who drowned crossing a lake that was 4-foot deep, on average. Let me explain…

Since the beginning of 2025, I’ve spoken with 150 – 200 people interested in financial advice. And last year, we referred more than 500 groups to financial advice.

Here’s what we found out about the true cost of financial planning fees and costs

Just in the past fortnight, I’ve undertaken 40 discovery calls with investors and business owners interested in Rask Advice.

Finally, after years of working alongside advisers, I can tell you – almost every Google result and “industry report” underestimates the true cost of holistic, end-to-end, comprehensive financial planning from a good firm.

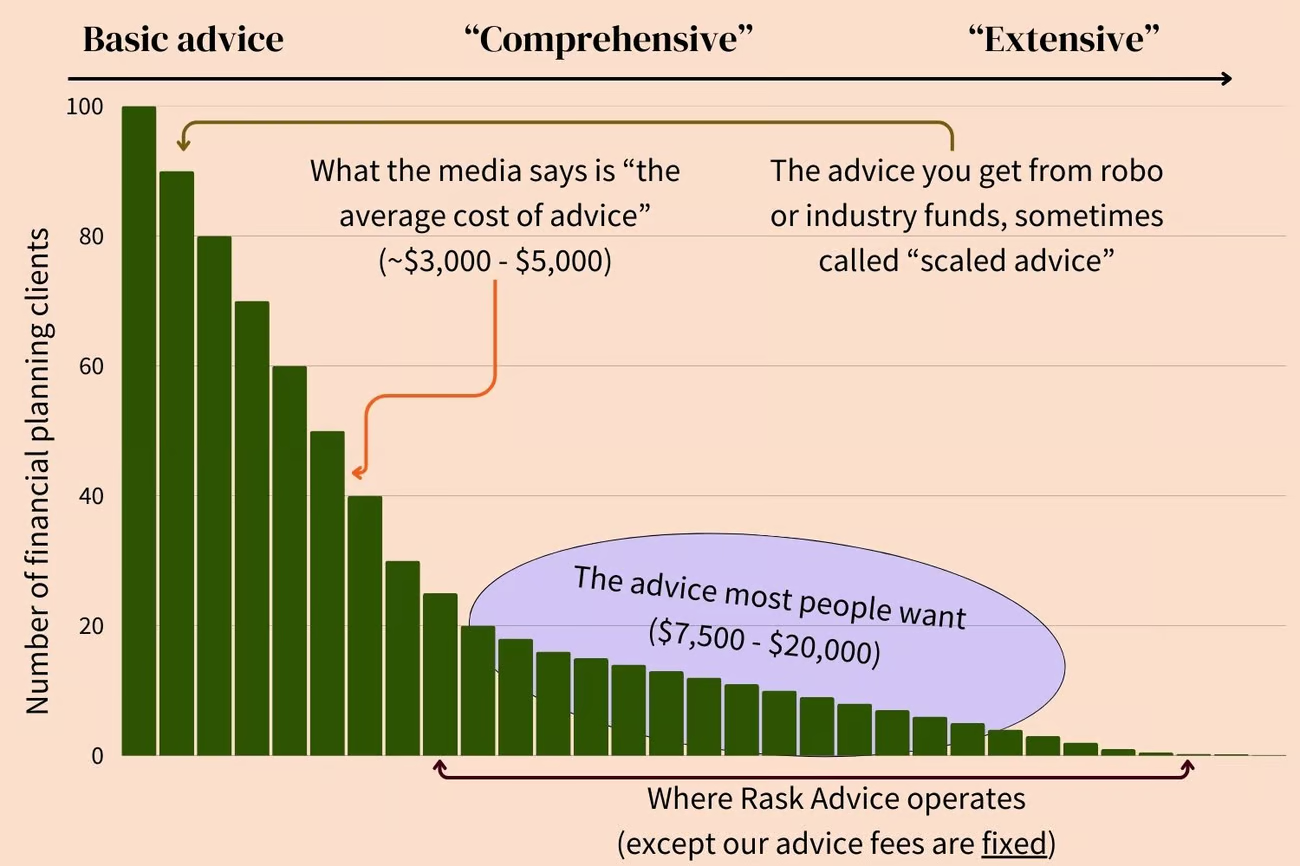

Here’s a chart I’ve come up with, to help you understand the nuance in the financial planning cost data:

The reality is, I estimate many financial advisers incur $3,000 in costs to do a (good) financial plan. So how could they offer a full planning service for less than that? Add in taxes and a little profit margin to create a sustainable business, and you’re looking at $5,000, just for the plan.

When should I get financial advice?

If it seems getting financial advice is a little expensive, when is it worth paying for?

Here are some of the times when getting financial advice makes sense.

- In the lead up to retirement – always. At retirement is when your nest egg is the largest it’ll ever be, you have more complex strategies available, you’re letting go of a salary, and more. In my experience, the most ‘at risk’ people at retirement age are the people who think they know what they’re doing. It’s overconfidence bias in action. After all, why would you risk $1 – 2+ million (and 20-30 years of returns) by not getting advice to simply double-check everything?

(Funny story – even Rask’s Head of Advice, Gemma Mitchell, has her own financial adviser!)

- When you want to achieve FIRE. This one surprised me. The largest number of people who have already signed up for our advice are people who are pursuing an early retirement – or those who have already achieved it and want to double-check the strategy. If you want to accelerate your path to wealth, it would make sense you get a financial plan and instructions from someone who has seen it dozens of times.

- When you receive an inheritance or insurance payout. Inheritances can be really complicated for tax reasons. But it’s the emotional reasons that impact decision making. After all, who wants to deal with complex tax returns and hundreds of thousands, or millions, of dollars when their loved one just passed away? Another big lump sum is a workplace injury, TPD & trauma payout, and so on. Sometimes your payout will include an allowance for financial advice.

(Note: we’re dealing with multiple people who have received inheritances recently. My advice: go slow.)

- When you have a passing interest in finance. If you’re not prepared to learn deeply about finance, get advice. Most people aren’t interested enough to DIY their finances successfully. If you haven’t read at least 10 finance books. Get advice.

- When you go through a divorce. Again, heightened emotions like anxiety, social pressure & fear can lead to bad outcomes. Test drive a few advisers to find a good fit.

- When you’re selling properties and have little stock market experience. The stock market, even with simple things like ETFs and industry Super funds, is not like property. Stocks may be better for true passive income + growth, but it’s a rollercoaster. So get advice, at least for the first year or two. If you’re unsure, think about it like this: many property investors pay real estate agents $50,000 to sell a property that would sell itself… but don’t pay $10k to a university qualified adviser to map out every part of their financial life for the next 10 years.

What can a financial adviser help with?

Typically, in a comprehensive financial advice firm, your adviser will address all of the key areas of your financial life, including cashflow and spending, superannuation, contributions, tax savings & entity structures, SMSFs, investments, estate planning, tax optimisation, lifestyle goals, and insurance.

Crucially, a financial adviser can help you plan and model your tax, but they’re not tax agents (i.e. they don’t do your tax return).

Key point: not all advice firms are created equally. The exact areas a firm can cover are detailed in its Financial Services Guide (FSG) and will be limited by the number of ‘authorisations’ of the licence (AFSL) it holds.

How do financial planning fees work?

Financial planning fees and costs can be a little tricky to work out. For one year of financial planning, many advice firms have fees that work like this:

- Upfront advice/plan: $4,000 – $20,000

- Ongoing service (typically starts at 30 days after #1): $4,000 – $30,000

- Implementation fee: $0 – $6,000

- Insurance commissions: 0 – 66% of the annual premium, then 0 – 22% each year after that.

The upfront fee covers the plan you receive. The ongoing fee is paid monthly and often pays for them to manage your portfolio. Many firms won’t do #1 without you committing to #2. The implementation fee covers the costs of them setting everything up for you.

At Rask Advice, we charge one fixed yearly advice fee. Pretty simple.

Is financial planning worth it?

So is financial planning even worth it? There are studies which show people who use an adviser invest better, make fewer mistakes, and so on.

However, most people still ask, “is financial planning worth it?”

If you’re in one of the six cases outlined, I think the chance of the advice being worthwhile is very good.

Where do people go wrong with financial advisers?

Most people go wrong when thinking about financial advice because:

- They compare the cost of advice to their portfolio size. This is a mistake because holistic or “comprehensive” financial advice explores every aspect of your financial life, not just your portfolio.

- They compare the cost to their yearly return. Some people think ‘if I pay $5,000 for advice, my return this year needs to improve by 2% to make it worth it.’ This is a mistake because the benefit of good financial advice will help you for many, many years to come. And oftentimes, the best part about seeing an adviser is not the returns, but the costly mistakes they help you avoid.

- They don’t read (and understand) the Financial Services Guide (FSG). The FSG is a required legal document that spells out exactly how a financial planning firm operates, the fees it charges, and so on. This should be available on the company’s website, usually in the footer/bottom.

- They don’t go into the meeting with a basic understanding of what they want. Before seeing an adviser, create a list of questions or simply have an idea of what you want from an adviser now and into the future.

- They don’t verify the financial adviser has a licence (AFSL), or acts under one. You can do this in one of two places: moneysmart.gov.au and service.asic.gov.au/search.

What are the steps in financial planning?

I’ll end this financial advice explainer by sharing the steps in financial planning.

Most personalised financial advice services, like ours, follow a similar process:

- You book a discovery call or video with the advice team.

- You complete an online fact-finding questionnaire. This is a detailed and extensive information gathering form that is required from you for them to make an informed judgement.

- A goal setting session takes place.

- The adviser presents the advice / your plan. After extensive modelling, your financial plan is prepared and presented to you.

- Implementation begins. Depending on your package, you may DIY a financial plan or the adviser’s team will “implement” it for you.

- An ongoing partnership begins. Often, these include quarterly, half-yearly or annual catch-ups with your advice team.

How long does financial advice take?

If you decide to get financial advice today, be prepared – the best financial advisers are in massive demand. Given the demand for good financial planners right now, from start to finish it can take 1-3+ months to receive your financial plan, get it going and have it in play.

For example, our financial advisers are extremely sought-after and always in high demand. Clients were paying deposits for financial advice in March, to likely receive their advice in June.

How to get started with financial advice

As you can see, financial planning fees and costs are a little more nuanced than you might expect. Fortunately, there are a few steps you can take:

- Shop around – the first meeting / call is often (but not always) free. Get a feel for it. Book in with us. Just have your key financial information and questions about the process ready.

- Read the FSG. Find our FSG here.

- Check the AFSL using the “Professional Registers” search engine on asic.gov.au.

- Don’t forget to ask plenty of questions!

Do all of that and I reckon it’ll be money well spent. The new breed of financial planners (post 2018) are absolutely wonderful – degree-qualified, ethical, skilful, trustworthy and transparent.